People who do not understand the Reverse Mortgage Purchase Strategy are missing out on a powerful solution to three common senior problems: (1) insufficient cash, (2) a broken monthly budget, and (3) living in a home that is less than ideal or just unsafe.

The centerpiece of this strategy is using a reverse mortgage as a purchase-money loan. You can’t say this is a misunderstood strategy because almost no one knows anything about it.

Below we'll cover five key points...

1) The 4 parts of the reverse purchase strategy

2) An example of the strategy

3) Who needs it and who is involved

4) How it benefits seniors

5) Demographic trends and opportunities

The 4-Part Reverse Purchase Strategy

1) Sell a house that doesn't fit - too big, two story, too expensive

2) Buy a better house with a HECM - no monthly mortgage payment

3) Invest or save excess sales proceeds to create a cash cushion

4) Minimize property taxes - e.g., TX tax freeze portability, CA Prop 60/90

Reverse Mortgage Purchase Loan

Before we go further, let’s quickly review reverse mortgage basics. It is a non-recourse loan, based on equity in a home, that does not get paid back until the last borrower sells or permanently leaves the house. If the house isn’t worth as much as the loan balance at the end, that’s not the borrower’s problem – the shortfall is forgiven.

The bank does not own the home or get the house, or any of the extra equity at the end. They only get paid back what was borrowed, interest and mortgage insurance (if FHA) that wasn’t paid throughout the years.

The borrower is allowed to sell or refinance the loan any time they like with no prepayment penalties or hidden fees.

The homeowner remains responsible for paying property taxes, homeowner insurance, and general maintenance. This responsibility (to pay ongoing property expenses) is true whether we’re talking about FHA loans that are insured by the federal government or the new Jumbo Reverse Mortgage that has lower closing costs and no mortgage insurance.

New jumbo reverse mortgage options allow people who are looking to buy a non-FHA-approved condo or a higher value home to take advantage of this strategy; i.e., finance part of a home purchase without having a monthly mortgage payment.

Most people think of a reverse mortgage as a way to access wealth from a home they already own. And most, including well-educated financial and legal professionals, do not know you can use a reverse mortgage to buy a home.

The home buyer does not have to pay cash for the house and then get a reverse mortgage – even if they’re buying a new-built home. There used to be a problem financing new construction because an application couldn’t be taken until the house had a certificate of occupancy. That was changed a few years ago.

A reverse purchase loan has the same terms, features, and functionality as a normal reverse mortgage – it’s the same loan. What’s also the same is that not everyone is eligible for a reverse mortgage.

Government changes over the last three years – designed to protect seniors – require not only considerable equity, but also good credit and adequate income to pay for housing expenses. I am happy to review anyone’s personal situation if they give me a call at (800) 208-1252.

Sometimes it’s easier to explain an unfamiliar strategy with an example or a case study.

Reverse Purchase Strategy Example

Many seniors have considerable wealth but it’s all tied up in their home and they can’t access it. We frequently hear comments like, “I’m rich on paper but I struggle financially each month.”

Another challenge we frequently encounter is people who are not eligible for a reverse mortgage on the home they live in. Usually that’s because they have too much debt or they owe more than 50% of the value of their home.

We talk to people who have homes worth $900,000 but they owe $550,000. This is often a house that’s too big; maybe the house they raised their kids in.

In their mind, they have $350,000 in equity. They’re confused and irritated when they learn they can’t get a reverse mortgage. But they would be eligible for a reverse mortgage on a less expensive home.

Here’s a fairly typical example. If your numbers are higher or lower, the concept is still the same.

Current Home

- 123 Main Street, Old Towne, USA

- Home purchased in 1990 for $250,000

- Existing mortgage balance $200,000

- House put on the market and sold for $850,000

- Selling commissions and fees total 6% or $50,000

- Net cash proceeds equal selling price minus loan payoff minus fees:

- 850,000 – 200,000 – 50,000 = 600,000

Next Home

- 345 Elm Street, New Town, USA

- Buyer has $600,000 cash from sale of Old Towne house

- Buyer finds new home at 345 Elm St, New Town, USA that they like better

- They successfully negotiate a price of $500,000

- The youngest buyer/borrower is 68

- They can borrow 45% of the value of the New Town house: 45% of $500,000 = $225,000

- Cash needed to close equals purchase price less new reverse mortgage of $225k

- 500,000 – 225,000 = 275,000

Outcome

- Borrower has cash left over from selling Old Towne property

- $600,000 (net sale proceeds) – $275,000 (cash for new house) = $325,000 (cash left over)

- Buyer’s new $500,000 home that fits their lifestyle better

- They have a reverse loan of $225,000, with no monthly mortgage payment

- They now have $325,000 more in their bank

- Better house + more money in the bank = better sleep + more smiles

Who Needs the Reverse Purchase Strategy?

When I teach this strategy, I often am asked, “So, who would need this or who should do this?” There are really two audiences for this message.

First, homeowners who can’t afford or don’t like where they live. Often, this conversation starts when we talk to adult children who are trying to figure out how to help their folks.

Second, financial planners with cash- or income-constrained clients, or financial planners who have clients that are exceeding a sustainable withdrawal rate. Conventional wisdom says a safe retirement account annual withdrawal rate is around 4.5%.

I get calls from financial planners who tell me they have clients who are taking out 10% of their portfolio each year. They and their clients know that is not sustainable. Often what’s necessitating these too-large withdrawals is the existing mortgage. Everyone dreams of going into retirement with no mortgage and lots of money in the bank; reality is usually or often otherwise.

People have existing mortgages in retirement because life happened along the way: maybe a job loss, health challenge, over-priced college tuition, wedding(s), helped kids buy their first home, etc. With taxes as high as they are, it’s not easy saving considerable money for retirement.

Who Is Involved in the Reverse Purchase Strategy?

This strategy involves multiple parties: a homeowner or renter, their families, a real estate agent, a reverse mortgage specialist, and those who act as financial advisors.

This strategy is not about taking money out of the house to invest. Rather, downsizing and freeing up trapped equity often results in excess cash that needs to be prudently managed to pay for future expenses and lifestyle.

Reverse Purchase Strategy Benefits

Money

The heart of this strategy revolves around our primary mission: helping people reduce financial distress that makes them feel isolated and insecure. Nothing is more rewarding than having a senior look you in the eye, thank you and say something like, “You’ve given us back our life, our independence, our joy.”

Because many people don't know about this strategy, their default advice is something along the lines of: you need to sell and rent. When possible, it is important that seniors retain appreciating assets as they age; i.e., they should own instead of rent if they're going to be in the home for a while.

In 2016, I wrote an article for The Reverse Review magazine where I talked about the $200,000 mistake of selling and renting. You can see the detail behind that research here: Rent or Own in Retirement.

Transamerica Center for Retirement Studies released an outstanding paper last year titled: A Precarious Existence: How Today’s Retirees Are Financially Faring in Retirement.

Unsurprisingly, the top factor in deciding whether to move and where to live when people are in or approaching retirement is affordability. The driver was money. Forty percent of retirees say paying off debt is a current financial priority. This is not surprising when you realize that 66% indicate Social Security will be or is their primary source of income.

Freeing up trapped wealth with the Reverse Purchase Strategy makes paying off debt (credit cards and installment debt) much easier.

While most people call this a downsizing strategy, downsizing may not mean a smaller house, it might mean a bigger (less expensive) house in another city or state. What got downsized was the monthly expenses. We’re actually starting a new division for people who may want or need to utilize this strategy in a less expensive state or city.

Half of the time, this strategy is about money (lowering overhead and increasing liquidity), the other half of the time it's about health, safety, and lifestyle.

Living in the Right House

Any of the following house characteristics are not a good fit, even if the homeowner can afford the house:

- An upstairs master bedroom (falling is a senior’s greatest risk)

- A large house or yard

- Increasing neighborhood crime

- Lack of nearby senior services or medical options

- Steep driveway or too many stairs

- Busy local streets

- No nearby relatives or good friends

People dealing with these situations often cannot pay afford to pay cash for a better-fitting home, nor do they qualify for a conventional mortgage because they don't have a job. The Reverse Purchase Strategy can be the perfect solution for people in this group.

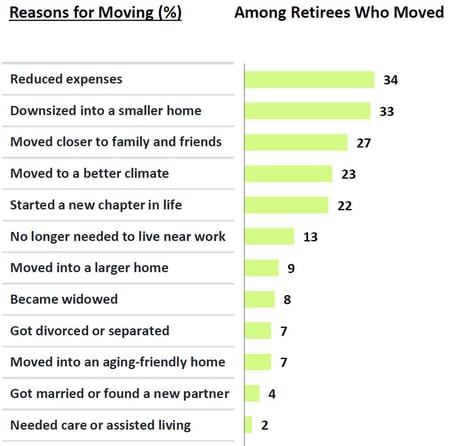

Why Retirees Move

The Transamerica Study charts below summarize why people move...

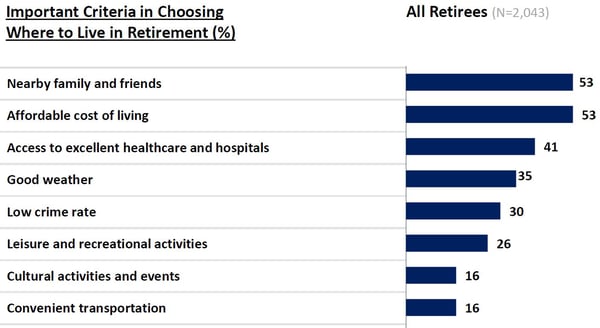

What’s Important to Retirees When Deciding Where to Live

Demographic Trends & Opportunities

Question: do you feel like there are more older people? It’s true and it is a global phenomenon. The United States currently has approximately 75,000 people who are age 100. By 2025, there will be 1 million people age 100+.

For the next 17 years, the U.S. will see 10,000 people per day pass age 65. Consider two questions:

1) How many retirees don't have enough money for a 20-yr unpaid vacation; i.e., retirement?

2) How many want or need to move for lifestyle, health, or safety reasons?

Most seniors, real estate agents, financial planners, and estate planning attorneys don’t know about the Reverse Purchase Strategy.

The following recent numbers show just how underutilized this approach is:

- There are roughly 5.9 million houses sold each year

- 80% of all urban and suburban buyers get a mortgage

- Reverse mortgage purchase loans (H4P) total 3,000 per year

- Only 6 out of 10,000 purchase loan are reverse mortgages

- That means, only 1 out of 2,000 homes sold last year used a reverse mortgage purchase loan

4.7 million people got a mortgage, only 3,056 used a reverse mortgage. The reason these numbers are so low is because so few people know this option exists.

That means there are...

Seniors who think they’re trapped, but they’re not.

Real estate agents who could sell more homes by solving problems, but they’re not.

Financial planners frustrated that their clients are going through their money too quickly, but it doesn’t have to be that way.

I get passionate when I think about reducing unnecessary suffering. These are safe, federal government-insured home loans. HUD/FHA introduced the reverse purchase loan in 2008. They were approved in TX in 2013.

The reverse purchase loan has been around for 5-10+ years. People don’t know that and they don’t understand this four-part strategy.

This represents opportunity looks like. This is what making a positive dent in the universe is about.

Summary

When we work with seniors, we keep in mind the truth that fear and joy cannot coexist.

Our senior clients tell us what they fear; they're afraid of living:

- In the wrong neighborhood – a place they used to love but no longer feel safe

- Away from loved ones who would be there when needed – if only they were closer

- In a house that isn’t safe or configured for seniors

A home equity solution (reverse mortgage) on a senior’s existing home won’t fix the items noted above. And if the senior lives in a house that’s too expensive, a reverse won’t help that either.

The Reverse Purchase Strategy can help get people into the right house and/or help them get into a more sustainable place financially.

By working with real estate agents and financial planners, we’re able to make retirees’ and seniors’ lives better, more meaningful, more productive. Anything that does all that is worth understanding and promoting.

If you know someone who might benefit from this strategy, please click the link below or have them go to www.ReverseLoanAmount.com. They can also call Kent Kopen at (800) 208-1252.

Resources | References:

- FHA Single Family Production Report, Office of Risk Management and Regulatory Affairs, Office of Evaluation, Reporting & Analysis Division, April 2019, HUD

- Number of Existing Homes Sold in the United States from 2005 to 2020, Jennifer Rudden, Mar 18, 2019, Statista

- Trading Economics, April 2019, U.S. Census Bureau

- Consumer Housing Trends Report 2018, Zillow Group

- The H4P Strategy, Kent Kopen, Nov 2016, The Reverse Review

- An Aging World: 2015, Wan He, Daniel Goodkind, Paul Kowal, March 2016, US Census Bureau

- Attitudes About Aging, 1/30/14, Pew Research Center

- Americans 55+ Housing Options Homeowners Data, June 2016, Freddie Mac GfK

- A Precarious Existence, Dec 2018, Transamerica Center for Retirement Studies

- Reverse Mortgages and Taxes, Kent Kopen, May 2017, The Reverse Advisor

- Tax-Freeze Portability, Mar 2018, Texas Realtors Legal FAQ

* Always review important financial decisions with your own legal and tax professionals.

About the Author

Kent Kopen earned his Reverse Mortgage Specialist credential in March 2007. In 2017, Kent earned the CRMP (Certified Reverse Mortgage Professional) designation. There are less than 200 CRMP designees in the United States. Mr. Kopen also provides education, tools, and strategies to professionals who offer financial and legal advice to others. "Our resources help financial advisors, CPAs, and estate planning attorneys help seniors optimize their home equity to provide greater security and peace of mind."

Kent Kopen earned his Reverse Mortgage Specialist credential in March 2007. In 2017, Kent earned the CRMP (Certified Reverse Mortgage Professional) designation. There are less than 200 CRMP designees in the United States. Mr. Kopen also provides education, tools, and strategies to professionals who offer financial and legal advice to others. "Our resources help financial advisors, CPAs, and estate planning attorneys help seniors optimize their home equity to provide greater security and peace of mind."